Many restaurant operators assume their payment provider’s compliance covers the whole business. It does not. If your restaurant takes card payments, PCI DSS – the Payment Card Industry Data Security Standard – applies to you, whether you run one site or twenty. That assumption often leaves gaps in restaurant payment security and PCI DSS compliance.

PCI is not a form problem. In restaurants, it is an environment design problem.

Most operators do not need the full standard explained line by line. They need clear answers to four practical questions: where card data enters the business, which systems sit in scope because of that, who has access to those systems, and which responsibilities sit with suppliers rather than the restaurant itself.

What PCI DSS covers in a restaurant

According to the PCI Security Standards Council merchant resources, PCI DSS applies to any entity that stores, processes, or transmits cardholder data (CHD), or sensitive authentication data (SAD), or could affect the security of either. In plain English, CHD means payment card information such as the card number and related account data, while SAD covers highly sensitive elements used to authenticate a payment, such as full magnetic-stripe data, card verification values, or PIN-related data.

That is why PCI in a restaurant is wider than the terminal on the counter. It can include pay-at-table devices, tills, point-of-sale (POS) systems, payment-connected back-office servers, remote support tools, online ordering journeys, and any workflow where staff can see or mishandle card data.

A typical restaurant estate can include:

- Fixed POS terminals at the bar or counter

- Handheld ordering and payment devices

- Online ordering or booking journeys

- Back-office machines connected to the payment environment

- Guest Wi‑Fi, staff devices and kitchen technology sharing the same physical site

This is exactly where operators get caught out. A terminal provider can be compliant in its own right, but that does not automatically make the restaurant compliant. A common failure could look like: a team member writes card details in a booking note for later entry, a delivery app is added to the same network as the POS, or a support supplier is given remote access that nobody reviews again. The PCI Security Standards Council is clear that scope still includes the systems and environments that store, process, transmit, or could impact cardholder data security. Encryption helps, and a validated point-to-point encryption (P2PE) solution can reduce scope significantly, but it does not remove PCI from the merchant environment altogether.

For a useful official starting point, the PCI Security Standards Council’s merchant resources explain the standard in merchant terms and give clear guidance on scope, self-assessment questionnaires, and common security failures.

Why PCI becomes painful in restaurants

The usual problem is not that restaurants ignore PCI. It is that they treat it as a yearly questionnaire instead of the result of how the payment environment has been designed. Operators working through the shift to v4.0.1 have also had to deal with updated validation expectations and new enforceable requirements, which is why clear guidance such as the PCI DSS v4.0.1 FAQ overview has become more useful, even if it is written for a broader merchant audience.

A site opens with one network. Guest Wi‑Fi gets added later. A delivery tablet appears. Remote access is given to a POS supplier. Another provider installs a support tool. Nobody redraws the map. By the time the self-assessment questionnaire arrives, the restaurant is trying to answer compliance questions about an environment nobody has fully documented.

PCI feels heavy when the environment is messy. The form is rarely the real problem. Operators are usually being asked to report on a payment setup that has grown in bits and pieces over time. The practical fix is simple: map the environment first, then simplify it.

Cardonet’s own article on restaurant POS security and PCI DSS compliance makes the same point from a network angle: flat networks, weak remote access, and poor segmentation are what turn routine payment estates into risky ones.

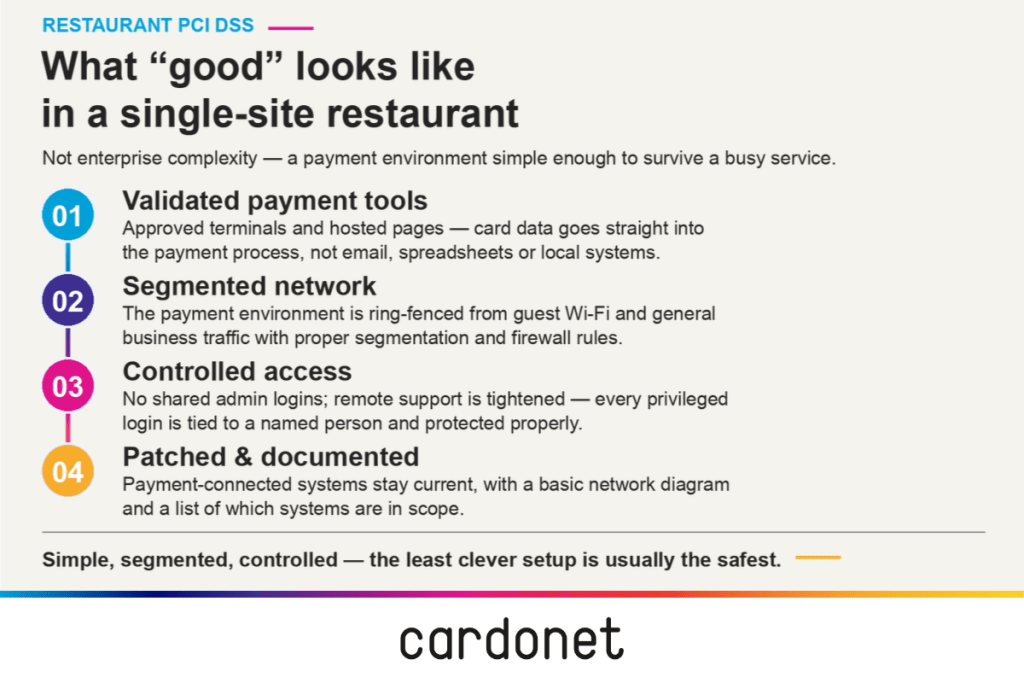

What good PCI looks like in a single-site restaurant

For a single-site operator, “good” does not mean enterprise-grade complexity. It means a payment environment that is simple, segmented, and controlled well enough to survive a busy service without shortcuts. The best single-site setups are usually the least clever ones from a restaurant POS security and PCI point of view with fewer systems touching payment data, fewer people with privileged access, and fewer workarounds added under pressure.

A sensible baseline usually comes down to four things:

- Use validated payment tools, such as approved terminals and hosted payment pages, so card details go straight into the payment process rather than wandering through email, spreadsheets or local systems.

- Separate the payment environment from guest Wi‑Fi and general business traffic with proper segmentation and firewall rules.

- Remove shared admin access and tighten remote support, so every privileged login is tied to a named person and protected properly.

- Keep payment-connected systems patched and documented, including a basic network diagram and a list of which systems are in scope.

This doesn’t sound like a lot but it solves most of the problems that make PCI awkward for independents. If card details are only ever entered into validated payment devices or hosted pages, if the payment network is ring-fenced, and if access is controlled properly, the assessment burden is usually far more manageable. Restaurant-facing guidance such as Paysafe’s PCI compliance for restaurants is useful here because it frames the issue in merchant terms rather than assessor jargon.

There are also a few habits worth stopping outright. Staff should not write down card details for later entry. Card numbers should not sit in booking notes. A supervisor should not lend a shared password because one person is off shift. And a back-office laptop used for payroll should not also become the machine someone plugs into the payment network because it is nearby. Restaurants tolerate these workarounds because service moves fast. PCI punishes them because they create avoidable exposure.

What breaks with PCI when you run multiple restaurant sites

For a multi-site group, the core controls are much the same. The real difficulty is consistency at scale. One site follows the current network template, another has legacy kit, a third has a local supplier workaround that head office has never documented properly, and a fourth opens with a slightly different payment flow because of local trading pressure. At that point, PCI is no longer just a security issue. It is a standards and change-control issue.

A more manageable group-wide position usually depends on three things:

- A repeatable site model for payments, POS, Wi‑Fi, segmentation and remote support

- A central record of what is in scope at each site and which suppliers can access it

- A rule that openings, refurbishments and major platform changes trigger a PCI review rather than being treated as separate projects

That matters for cost as much as compliance. When sites share a standard design, support is faster, assessments are easier to prepare, and changes are less likely to create accidental scope. In practice, multi-site PCI is not about adding layers of policy. It is about reducing variation across the estate.

This is where outside support becomes useful. Cardonet’s restaurant IT support page is relevant because the operational challenge is not just understanding the standard. It is keeping payment, network and support disciplines consistent across service hours and across sites.

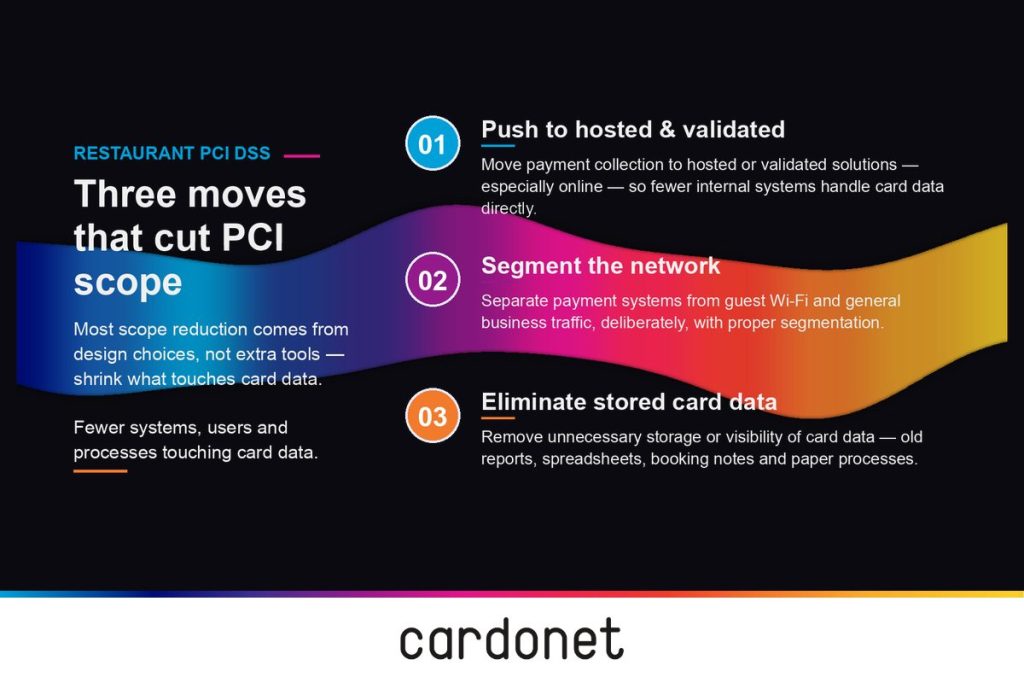

How to reduce PCI scope without cutting corners

A lot of PCI advice gets bogged down because it starts with every requirement in the standard rather than with scope. The cleaner question is simpler: how can the restaurant reduce the number of systems, users and processes that ever touch cardholder data? Most of the heavy lifting in PCI scope reduction comes from design choices, not extra tools.

Three moves tend to matter most:

- Push payment collection towards hosted or validated solutions wherever sensible, especially online, so fewer internal systems handle card data directly.

- Segment the network deliberately so payment systems are separated from guest and general business traffic.

- Eliminate unnecessary storage or visibility of card data, whether that means old reports, spreadsheets, booking notes, or paper processes that should have disappeared years ago.

One nuance is worth spelling out clearly. Encryption is important, but the PCI Security Standards Council states that encryption on its own does not automatically take an environment out of scope. Merchants still need to consider where cardholder data exists, which systems perform encryption or decryption, where keys are managed, and whether those systems remain accessible inside the environment. Broader merchant guidance on reducing PCI DSS scope is useful here because it explains why segmentation and scope control often matter as much as encryption itself.

Where operators usually need outside help on PCI and payment security

A good restaurant IT partner should make PCI easier to operate, not harder to understand. That means mapping the payment flow, documenting what is in scope, separating networks properly, tightening remote access, and making sure responsibilities are clear between the restaurant, the acquirer, the payment provider, the POS supplier and the IT support team.

The PCI Security Standards Council is explicit that merchants need to understand the split between their own responsibilities and those of service providers. That is one of the biggest gaps in restaurant environments. Operators are often told a platform is compliant, then assume the whole payment chain is covered. It is not. Your provider may secure their platform. You still own your side of the environment.

For a single site, that means simplicity and discipline. For a group, it means consistency and control across the estate. Either way, the value of the right support is that PCI becomes part of normal operations rather than a separate annual panic. If you need help with the day-to-day controls behind that, Cardonet’s cyber security services page outlines the operational work involved: access control, monitoring, support discipline, and clear ownership.

The practical next step on PCI DSS in your restaurant

Do not start with the questionnaire. Start with a map. List every way the business takes payments, every system involved in those journeys, every remote access route into them, and every place cardholder data or sensitive authentication data could be stored, exposed or mishandled.

If you only do three things this quarter:

- Map the full payment flow across in-venue, online and phone payments, then identify which systems are genuinely in scope.

- Fix the basics around network separation and privileged access before spending money on extra tools.

- Get clear, in writing, on which PCI responsibilities sit with your restaurant and which sit with your providers.

That exercise usually tells you whether the environment is clean or whether scope has drifted. Once you have that view, the next priorities are usually obvious: simplify the payment flow, tighten access, separate the network, and remove any unnecessary handling of card data. For a broader Cardonet view on why this works operationally, the insight on cyber security as a product of operational excellence is a useful companion read.

The operators who handle PCI best do not treat it as a yearly obligation. They design it into the way the business runs. Done properly, PCI protects revenue, guest trust and service continuity.

The next move is straightforward: review your payment flow, your site network, and your supplier access before the next compliance cycle forces the issue. Cardonet can help restaurant operators turn that review into a practical PCI scope and payment security plan, whether the challenge is one site that has grown messily or a multi-site estate that needs consistency across every location.

FAQs

1. I only have one restaurant. Do I really need to worry about PCI DSS?

Yes. If you take card payments in any form, PCI DSS applies, even for a single neighbourhood site. The aim is not to build enterprise security but to keep card data away from most of your systems and concentrate protection on the small part of your environment that actually needs it.

2. My POS or payment provider says they’re PCI compliant. What’s still on me?

Their PCI status covers their own platform, not your whole setup. You are still responsible for how your network is designed, how POS and payment devices are segmented from guest Wi‑Fi and general traffic, how remote access into your environment is controlled, and whether staff ever see, write down or store card details outside the payment flow.

3. As a single-site operator, what are the first three things I should fix?

Focus first on design, not tools. Use approved payment terminals and hosted payment pages so card details go straight into those systems rather than through email or spreadsheets. Put POS and payment equipment on a separate, protected network from guest Wi‑Fi and general devices. Replace shared “manager” logins with named accounts and tighten any remote support access so you always know who can reach your payment environment.

4. I run several sites. How do I stop PCI turning into a mess?

The key is to standardise rather than letting each site improvise. Agree one pattern for how payments, POS and Wi‑Fi are set up and apply it everywhere. Keep a central view of which systems and suppliers are in scope at each location so there are no surprises when assessments come around. Treat new openings, refurbishments and major tech changes as PCI events by default, not as separate local projects that bypass the group standard.

5. What should a good IT partner actually do for PCI?

A useful IT partner turns PCI into a routine part of running your technology, not an annual panic. In practice, that means mapping how card data flows through your business, documenting which systems are in scope, designing and maintaining proper separation between payment systems and everything else, and locking down remote access so only the right people and suppliers can reach sensitive systems. They should also help you keep responsibilities straight between you, your acquirer, your payment provider, your POS vendor and your own support team, so there are no grey areas where everyone assumes someone else is handling PCI.

You must be logged in to post a comment.